Definition

Value chain analysis (VCA) is a process where a firm identifies its primary and support activities that add value to its final product and then analyzes these activities to reduce costs or increase differentiation.

Value chain represents the internal activities a firm engages in when transforming inputs into outputs.

What is Value Chain Analysis

Value chain analysis is a strategy tool used to analyze internal firm activities. Its goal is to recognize which activities are the most valuable (i.e., are the source of cost or differentiation advantage) to the firm and which ones could be improved to provide competitive advantage.

In other words, by looking into internal activities, the analysis reveals where a firm’s competitive advantages or disadvantages are. The firm that competes through differentiation advantage will try to perform its activities better than competitors would do.

If it competes through cost advantage, it will try to perform internal activities at lower costs than competitors would do. When a company is capable of producing goods at lower costs than the market price or to provide superior products, it earns profits.

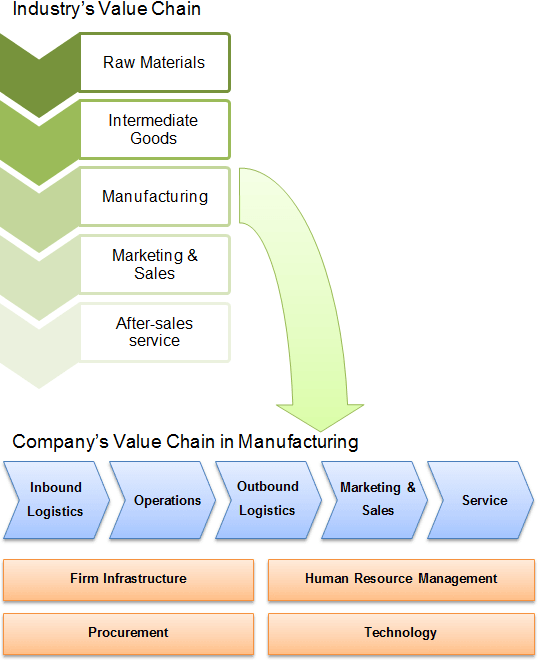

M. Porter introduced the generic value chain model in 1985. Value chain represents all the internal activities a firm engages in to produce goods and services. VC is formed of primary activities that add value to the final product directly and support activities that add value indirectly.

Although primary activities add value directly to the production process, they are not necessarily more important than support activities. Nowadays, competitive advantage mainly derives from technological improvements or innovations in business models or processes. Therefore, such support activities as ‘information systems’, ‘R&D’ or ‘general management’ are usually the most important source of differentiation advantage.

On the other hand, primary activities are usually the source of cost advantage, where costs can be easily identified for each activity and properly managed.

A firm’s VC is a part of a larger industry’s VC. The more activities a company undertakes compared to the industry’s VC, the more vertically integrated it is. Below, you can find an industry’s value chain and its relation to a firm-level VC.

Using the tool

There are two different approaches on how to perform the analysis, which depend on what type of competitive advantage a company wants to create (cost or differentiation advantage). The table below lists all the steps needed to achieve cost or differentiation advantage using VCA.

Competitive advantage types

| Cost advantage | Differentiation advantage |

|---|---|

| This approach is used when organizations try to compete on costs and want to understand the sources of their cost advantage or disadvantage and what factors drive those costs. (good examples: Amazon.com, Walmart, McDonald’s, Ford, Toyota) | The firms that strive to create superior products or services use a differentiation advantage approach. (good examples: Apple, Google, Samsung Electronics, Starbucks) |

|

Step 1. Identify the firm’s primary and support activities. Step 2. Establish the relative importance of each activity in the total cost of the product. Step 3. Identify cost drivers for each activity. Step 4. Identify links between activities. Step 5. Identify opportunities for reducing costs. |

Step 1. Identify the customers’ value-creating activities. Step 2. Evaluate the differentiation strategies for improving customer value. Step 3. Identify the best sustainable differentiation. |

Cost advantage

To gain a cost advantage, a firm has to go through 5 analysis steps:

Step 1. Identify the firm’s primary and support activities. All the activities (from receiving and storing materials to marketing, selling and after-sales support) that are undertaken to produce goods or services have to be clearly identified and separated from each other. This requires an adequate knowledge of the company’s operations because value chain activities are not organized in the same way as the company itself. The managers who identify value chain activities have to look into how work is done to deliver customer value.

Step 2. Establish the relative importance of each activity in the total cost of the product. The total costs of producing a product or service must be broken down and assigned to each activity. Activity-based costing is used to calculate costs for each process. Activities that are the major sources of cost or done inefficiently (when benchmarked against competitors) must be addressed first.

Step 3. Identify cost drivers for each activity. Only by understanding what factors drive the costs can managers focus on improving them. Costs for labor-intensive activities will be driven by work hours, work speed, wage rate, etc. Different activities will have different cost drivers.

Step 4. Identify links between activities. Reduction of costs in one activity may lead to further cost reductions in subsequent activities. For example, fewer components in the product design may lead to fewer faulty parts and lower service costs. Therefore identifying the links between activities will lead to a better understanding of how cost improvements would affect the whole value chain. Sometimes, cost reductions in one activity lead to higher costs for other activities.

Step 5. Identify opportunities for reducing costs. When the company knows its inefficient activities and cost drivers, it can plan on how to improve them. Too high wage rates can be dealt with by increasing production speed, outsourcing jobs to low-wage countries or installing more automated processes.

Differentiation advantage

VCA is done differently when a firm competes on differentiation rather than costs. This is because the source of differentiation advantage comes from creating superior products, adding more features and satisfying varying customer needs, which results in higher cost structure.

Step 1. Identify the customers’ value-creating activities. After identifying all value chain activities, managers have to focus on those activities that contribute the most to creating customer value. For example, Apple products’ success mainly comes not from great product features (other companies have high-quality offerings, too) but from successful marketing activities.

Step 2. Evaluate the differentiation strategies for improving customer value. Managers can use the following strategies to increase product differentiation and customer value:

- Add more product features;

- Focus on customer service and responsiveness;

- Increase customization;

- Offer complementary products.

Step 3. Identify the best sustainable differentiation. Usually, superior differentiation and customer value will be the result of many interrelated activities and strategies used. The best combination of them should be used to pursue sustainable differentiation advantage.

Value Chain Analysis Example

This example is partially adopted from R. M. Grant’s book ‘Contemporary Strategy Analysis’ p.241. It illustrates the basic VCA for an automobile manufacturing company that competes on cost advantage. This analysis doesn’t include support activities that are essential to any firm’s value chain; thus the analysis itself is not complete.

| Step 1 – Firm’s primary activities | |||||

| Design and engineering | Purchasing materials and components | Assembly | Testing and quality control | Sales and marketing | Distribution and dealer support |

|---|---|---|---|---|---|

| Step 2 – Toal cost and importance | |||||

| $164 M less important | $410 M very important | $524 M very important | $10 M not important | $384 M important | $230 M less important |

| Step 3 – Cost drivers | |||||

| Number and frequency of new models Sales per model | Order size Average value of purchases per supplier Location of suppliers | Scale of plants Capacity utilization Location of plants | Level of quality targets Frequency of defects | Size of advertising budget Strength of existing reputation Sales Volume | Number of dealers Sales per dealer Frequency of defects requiring repair recalls |

| Step 4 – Links between activities | |||||

| High-quality assembling process reduces defects and costs in quality control and dealer support activities. Locating plants near the cluster of suppliers or dealers reduces purchasing and distribution costs. Fewer model designs reduce assembling costs. Higher order sizes increase warehousing costs. | |||||

| Step 5 – Opportunities for reducing costs | |||||

| Create just one model design for different regions to cut costs in designing and engineering, to increase order sizes of the same materials, to simplify assembling and quality control processes and to lower marketing costs. Manufacture components inside the company to eliminate transaction costs of buying them in the market and to optimize plant utilization. This would also lead to greater economies of scale. | |||||

Sources

- Grant, R.M. (2010). Contemporary Strategy Analysis. 7th ed. John Wiley & Sons, p. 239-241

- Wikipedia (2013). Value Chain. Available at: https://en.wikipedia.org/wiki/Value_chain

- NetMBA (2010). Value Chain.

Is McDonald’s Competitive Advantage sustainable in today’s fast-evolving market landscape? How does the company’s management of tools and resources contribute to its success in the industry?